Borrowers who were misled or defrauded by their schools and ended up with private student loans – especially those issued by Sallie Mae/Navient between 2002 and 2014 – face an uphill battle in seeking debt relief. Unlike federal loans (which have a Borrower Defense to Repayment program), private loans have no comparable government-run discharge program. Navient (formerly Sallie Mae) has quietly implemented its own “School Misconduct Discharge” program for private loans, but reports show it has been opaque and largely unhelpful to borrowers. Below, we summarize what is known about Navient’s handling of these discharge applications (including denial rates and investigations), explain legal grounds and differences from federal loan protections, and outline options for affected borrowers. We also highlight recent lawsuits, regulatory actions, and what reforms may be on the horizon. The goal is to provide clear, actionable insights for borrowers seeking relief.

Navient – one of the largest private student loan holders – created a little-known program in early 2024 allowing borrowers to apply for cancellation of private loans if their school engaged in fraud or misconduct. Notably, Navient did not publicize this program; it was “quietly released” and only came to light through advocacy groups and media reports. Under this School Misconduct Discharge Application process, borrowers submit evidence that their school misled them or violated laws, and Navient then decides whether to discharge the private loan debt.

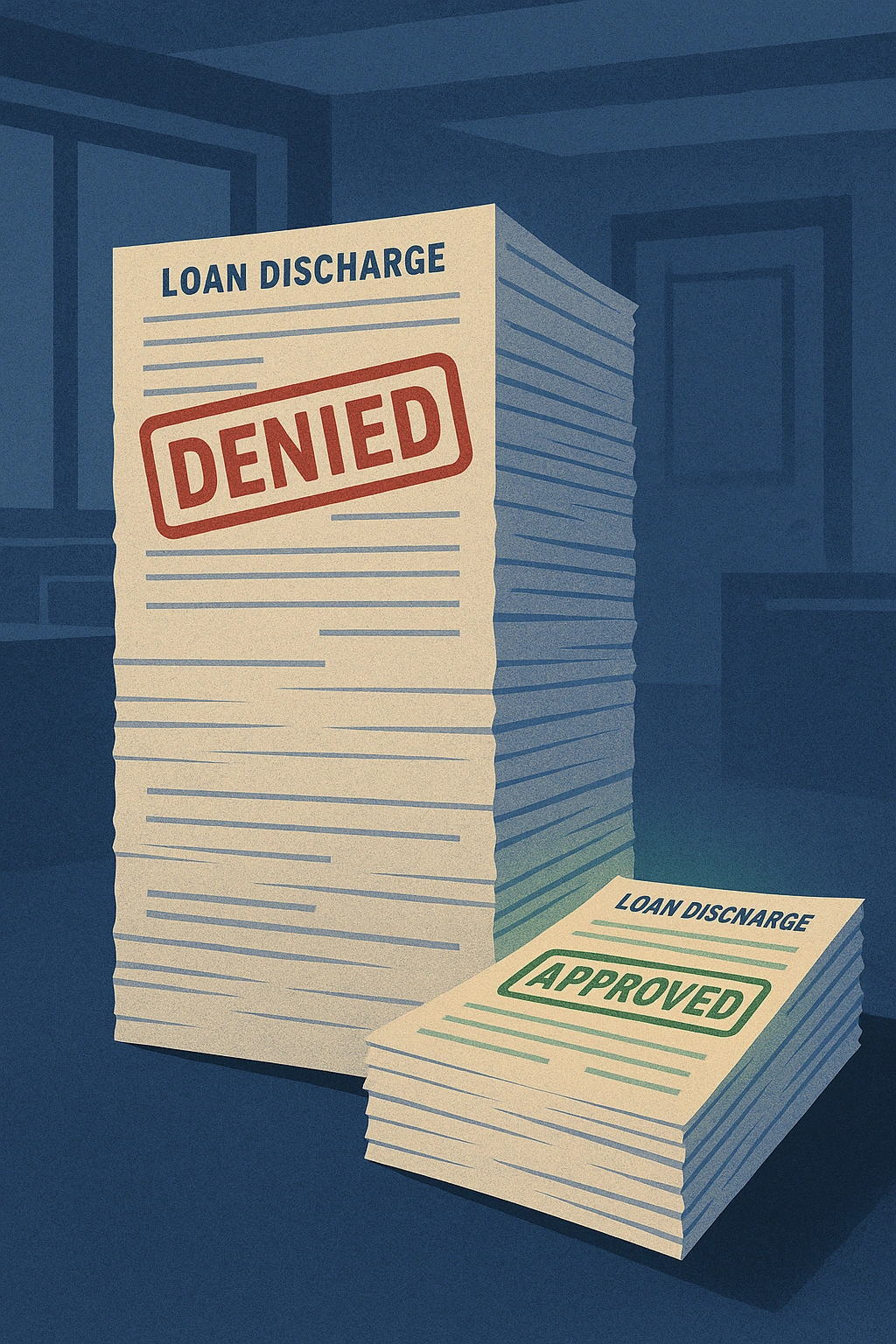

In late 2024, Senator Elizabeth Warren and colleagues launched a congressional inquiry into Navient’s handling of these applications. They found that Navient only invited a small fraction of eligible borrowers to apply, and then denied relief to about 80% of those who did apply. Specifically, Navient told Congress that as of September 2024 it had identified about 65,000 borrowers who attended for-profit colleges in its private loan portfolio, yet had sent out only 4,233 discharge applications to borrowers. Of those, 1,801 borrowers submitted applications, and Navient “fully reviewed” 1,061 cases – approving only 238 and denying 823. In other words, roughly 77–80% of applicants were denied, and less than 1 in 10 potentially eligible borrowers even got the chance to apply. Lawmakers characterized this outcome as “disgraceful”, suggesting Navient is “improperly denying thousands of borrowers relief” that they are entitled to by law.

Borrowers who went through Navient’s process have described it as opaque and frustrating. Navient’s application form is 12 pages long and demands extensive documentation – asking borrowers to recall when they discovered the school’s wrongdoing and to produce decades-old evidence such as school catalogs, marketing materials, or court judgments against the school. The form even warns that incomplete information could be deemed perjury. Despite this burden on borrowers, Navient’s denial notices provide virtually no explanation. In many cases, borrowers received only a generic form letter stating that the request was denied after a “holistic” review, without identifying any specific criteria that caused the denial. If borrowers attempt to dispute or appeal the denial, Navient responds with boilerplate language that it cannot provide details because the review is “holistic”. According to a recent lawsuit, Navient “mass-denied applications with cursory and boilerplate language” and then refused to explain its decisions, calling its evaluation process “proprietary and confidential”. In short, borrowers are left in the dark about why their discharge was refused and have no clear guidance on how to fix or appeal it.

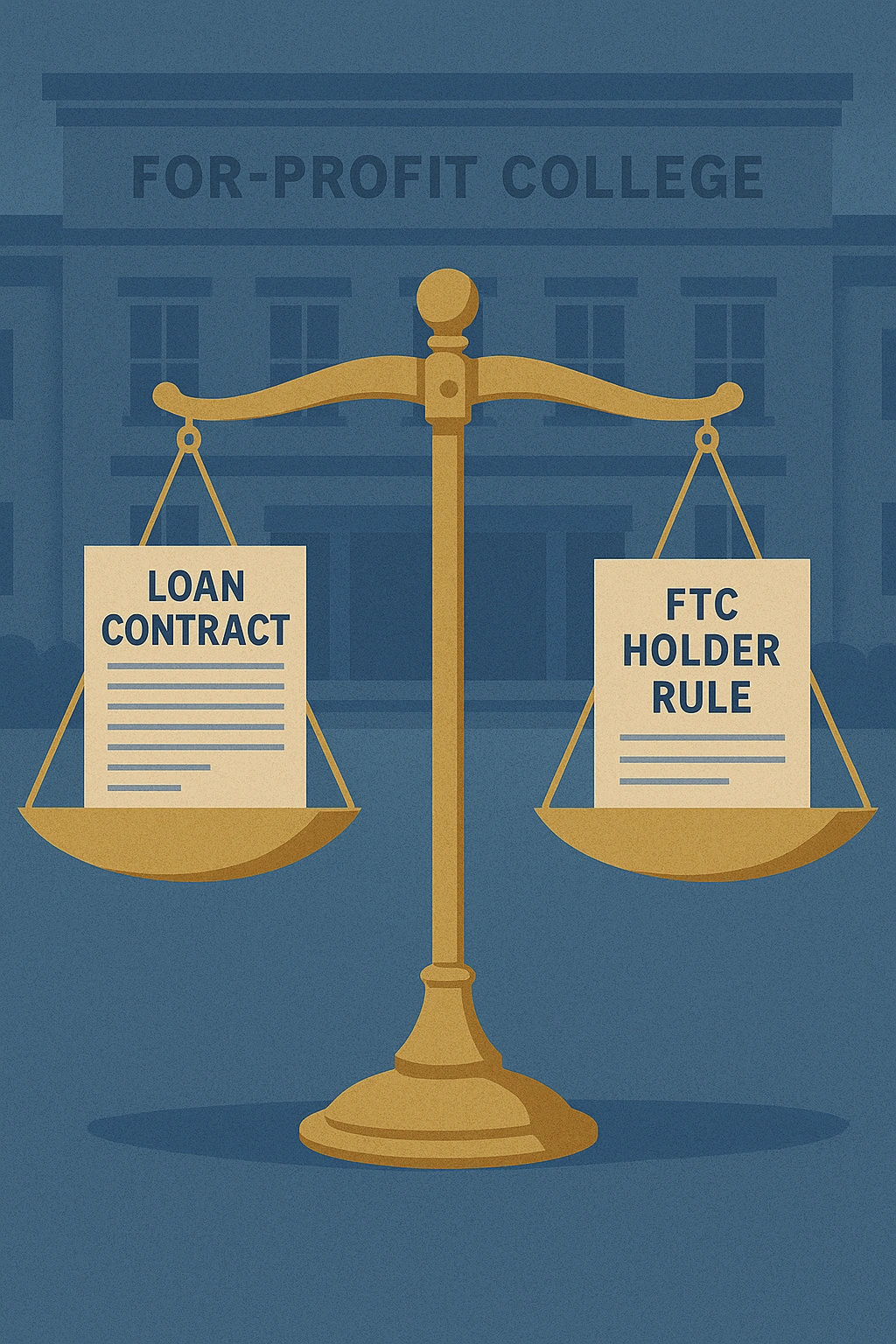

These revelations have prompted public officials to take action. In December 2024, Sen. Warren (joined by 24 other members of Congress) sent a letter to the Consumer Financial Protection Bureau (CFPB) and Federal Trade Commission (FTC) detailing Navient’s conduct and urging an investigation. “Navient’s cancellation process for borrowers who attended predatory, for-profit schools is flawed and opaque and potentially violates federal consumer protection law,” the lawmakers wrote. They noted that Navient had promised to cancel all private loans that meet the criteria of the FTC’s Holder Rule (see below), yet “the convoluted process the company has set up for defrauded borrowers is flawed” and “Navient denies relief to 80%” of applicants, often with improper or opaque reasoning. The letter called Navient’s behavior “disgraceful” and urged the CFPB and FTC to use their enforcement powers to ensure borrowers get the relief “they are entitled to under the Holder Rule”.

Regulatory findings echo these concerns. In a December 2024 report, the CFPB highlighted that some student loan servicers “misled borrowers about their right to challenge their loans” and failed to properly consider most borrower claims of school misconduct, effectively denying borrowers the protections that exist in law. This aligns with what borrowers and advocates have reported about Navient’s secretive program: despite having a contractual duty to consider school fraud claims, the company has been dodging that responsibility. As Eileen Connor, an attorney with the Project on Predatory Student Lending, summed up, “Student borrowers have legal rights to loan cancellation when there is evidence of fraud, and Navient has not been fulfilling its duty under the law.”.

The focus on loans from 2002 to 2014 is no accident. During this period, Sallie Mae (the predecessor of Navient) partnered with many for-profit colleges to issue private “subprime” student loans to high-risk borrowers. These loans often carried high interest rates and were “designed to fail,” with Sallie Mae fully aware that many students would be unable to repay them. Why would a lender knowingly make loans likely to default? Investigations and lawsuits have shown a quid pro quo arrangement: for-profit schools needed private loan funds to keep accessing federal aid, and Sallie Mae wanted a pipeline of federally-guaranteed loans. Under the federal 90/10 rule, for-profit colleges must get at least 10% of their revenue from non-federal sources – so these schools aggressively pushed private loans to cover that gap. Sallie Mae “collaborated with for-profit schools” to serve this need, treating the risky private loans as a “baited hook” to reel in more profitable federal loan business. In essence, the schools got the benefit of students’ tuition funded by private credit, and Sallie Mae/Navient profited on both ends (the private loans, which were often cosigned or otherwise insured by the schools, and the federally-backed loans the students also took).

For example, a recent Illinois lawsuit describes how a financial aid counselor at the now-defunct International Academy of Design and Technology (IADT) urged the plaintiff to take out private Sallie Mae loans – with variable interest and fewer protections – even though she was eligible for federal Stafford loans. The counselor downplayed the risks, falsely assuring her “you’ll be making more than enough money once you graduate to pay this off.” In reality, the school’s credits were non-transferable and job prospects never materialized. This bait-and-switch was common at certain for-profit colleges: students were promised great outcomes, “enticed to enroll” by deceptive claims, and then saddled with high-cost private debt.

The fallout from these practices is enormous. Many of these private loans had astronomical default rates (in some cohorts, 50–90% of borrowers defaulted), reflecting how untenable they were for the students. Even when borrowers managed to avoid default by making payments, they often found their balances ballooning due to interest and fees. (Indeed, a cruel irony noted in one case: a borrower who diligently paid for years saw her balance grow from $61k to $86k, and was excluded from earlier relief programs precisely because she hadn’t defaulted.)

In January 2022, a coalition of 39 state attorneys general reached a $1.85 billion settlement with Navient over these predatory lending practices. As part of that deal, Navient canceled about $1.7 billion in private loan balances for roughly 66,000 borrowers nationwide. However, the relief was targeted to a narrow group – primarily borrowers who had already defaulted on certain subprime private loans (many of which were disbursed between 2002 and 2014). Borrowers who kept struggling to pay (or who defaulted after the cutoff date) were not included. This means hundreds of thousands of borrowers from that era still carry these loans. Navient’s new “school misconduct” discharge program is ostensibly a way to help those left behind, but as detailed above, it has provided relief to only a tiny fraction so far.

If you have a private student loan from the early 2000s through mid-2010s that you believe was connected to school fraud (common examples include loans for Corinthian Colleges, ITT Technical Institute, Art Institutes, Career Education Corp schools like IADT, DeVry University, etc.), know that you are not alone. There is a history of systemic misconduct behind these loans, and both your school and the lender may have been complicit. This context strengthens the case that your debt is legally challengeable – even if Navient is currently stonewalling many borrowers.

Borrowers with private loans tied to school misconduct have several legal grounds on which they can seek relief or cancellation of their debt. Key theories include:

In practical terms, these legal grounds often get tested when a borrower stops paying and gets sued by the lender or debt collector. At that point, the borrower can raise the Holder Rule and school misconduct as an affirmative defense, potentially getting the debt declared void. However, waiting for a lawsuit is obviously risky and damaging (to credit, etc.). This is why advocates pushed Navient to create a proactive application process – so borrowers could assert these rights without having to default first. Unfortunately, as we’ve seen, Navient’s process has been adversarial and resistant to granting relief.

How This Differs from Federal Borrower Defense: It’s important to understand that the legal rights described above exist independently of the federal loan system’s Borrower Defense program. Borrower Defense to Repayment (BDR) is a U.S. Department of Education regulation that allows federal student loan borrowers to apply to have their loans forgiven if their school deceived them or broke certain laws. If a BDR claim is approved, the government cancels the federal loan and usually attempts to recoup the loss from the school. However, BDR applies only to federal loans – not private loans. So, if you were steered into a private loan instead of a federal loan, you effectively lost access to this federal safety net. There is no “official” borrower defense program for private loans managed by any government agency.

This means that for private loans, the onus is on the borrower to pursue relief through contracts and courts, rather than through an administrative claim. If you had taken a federal loan and your school lied to you, you could file a BDR application with the Department of Education and potentially receive a full discharge from the government (as many students from Corinthian, ITT Tech, etc. have). By contrast, with a private loan, you must appeal to the lender (as with Navient’s misconduct discharge form) or raise the issue in a legal forum. The protections differ as well: Federal loans have additional benefits like closed-school discharge (if your school shut down before you could finish, the federal loan can be forgiven) and public service forgiveness, etc. Private loans typically lack these guarantees. The Borrower Defense program has also evolved to allow group discharges – the Department of Ed can forgive whole groups of students’ loans if a pattern of fraud is proven, without each student needing to individually apply. No private lender offers an equivalent group relief mechanism; at best, they respond to class-action lawsuits or settlements after the fact.

In summary, borrowers with private loans have to rely on contract and state-law remedies, whereas federal loan borrowers can lean on specific Department of Ed programs. The substantive grounds (misrepresentation, etc.) are very similar – in fact, BDR claims themselves are typically based on a violation of state law by the school – but the process and enforcement are completely different. Navient’s so-called School Misconduct Discharge program is effectively a private, voluntary analog to Borrower Defense, but it operates with none of the transparency or borrower-friendly presumptions that the federal program aspires to. Navient is acting as both “judge and jury” on these private discharge claims, whereas with federal loans an impartial government process (imperfect though it may be) decides the outcome.

If you are a borrower stuck with a private student loan from a predatory school, there are several paths you can pursue now. These include legal action (individually or as a group), regulatory and oversight channels, and other strategies to protect your rights. We’ll outline each, along with recent developments that might support your efforts:

Action: If you haven’t yet submitted a School Misconduct Discharge Application to Navient, consider doing so – with tempered expectations. Navient’s application form can be obtained (PPSL has posted a blank copy on their website). The form will require you to detail the misconduct by your school and provide any supporting documentation. Be as thorough as possible: include specifics of what the school misrepresented to you, and attach copies of any evidence (emails, brochures, news of law enforcement actions against the school, etc.). If you know of government investigations or lawsuits against your school, mention them. Navient has asked for things like school catalogs and even court judgments, which many borrowers won’t have; still, provide what you can.

What to expect: Unfortunately, as detailed, the odds of approval are low – Navient has been denying ~80% of applications and often does not explain why. Some borrowers report being denied even when their school (e.g. Corinthian Colleges or ITT Tech) is a well-known case of fraud. Navient’s process has been inconsistent and opaque. If you do get denied, you can try to appeal or reapply if you have new evidence, but Navient’s own communications suggest the appeals process is limited and they often give the same boilerplate reply.

Why bother then? Two reasons: (1) Filing puts your situation on record. It creates documentation that you asserted your rights. If regulators later crack down on Navient or if a class action is certified, those records could help identify you as eligible for relief. (2) In the best case, you might be among the minority who do get their loans canceled. Navient claimed it has approved 238 borrowers as of last fall – some borrowers have indeed had their private loans forgiven through this program. It likely depends on the exact criteria Navient is using (which they haven’t fully disclosed). It could be that only the most clear-cut cases (e.g. certain loans from specific programs) are being approved. There’s a chance your case fits whatever mold they are reluctantly accepting.

Important: When filling out Navient’s form, stick to factual statements and avoid exaggeration. Any intentional falsification could cause trouble (the form is under penalty of perjury). If you’re unsure how to answer a question (for example, “when did you discover the misconduct” or describing the impact on your life), answer honestly in your own words – there’s no “wrong” answer about your personal experience, but they may be assessing credibility and thoroughness.

Given Navient’s track record, you should prepare for the possibility that you’ll need to fight through legal channels. Start by organizing your documents: loan promissory notes, any emails or letters from the school, promotional materials you received, your enrollment agreement, transcripts, etc. Also try to write down a timeline of events (when you enrolled, what you were told and by whom, when you first realized something was wrong, etc.). This will be incredibly useful if you later join a lawsuit or have to present your case to an attorney/general or judge.

Seek a consultation with a student loan lawyer or consumer protection attorney, especially one familiar with for-profit college cases. Nonprofit legal organizations like the Project on Predatory Student Lending (PPSL), legal aid societies, or state attorney general offices may be interested in your case if your school was notorious. PPSL, for example, has actively been litigating against Navient on behalf of borrowers from predatory schools. They and similar groups often collect borrower stories to identify patterns of misconduct.

If you can find other former students from your school who also have private loans, band together. Class action lawsuits can be a powerful tool when many borrowers share the same grievance. In February 2025, an Illinois borrower who attended IADT filed a class-action lawsuit against Navient for arbitrarily denying discharge applications despite clear evidence of school fraud. Her suit alleges that Navient’s blanket denials violate consumer protection laws and seeks relief for all Illinois borrowers who were similarly denied. This is a state-level class action – a model that could be replicated in other states or nationally (via a federal class action) depending on the circumstances. If such a lawsuit exists in your state or involving your school, you may be able to join as a class member or at least benefit if it succeeds.

Example: Amanda Luciano, the named plaintiff in the Illinois case, accrued loans for a “worthless degree” at IADT. After the big 2022 Navient settlement, her loans weren’t canceled because she hadn’t defaulted (she kept paying to protect her credit). Navient later sent her a misconduct discharge application, which she submitted with evidence of IADT’s “widespread fraud.” Yet she got a form denial with no explanation. According to her complaint, Navient denied her and others with only “boilerplate” reasons and refused to clarify, calling the process confidential. Her lawsuit seeks not only to force Navient to give a fair review or discharge to borrowers, but also to compensate borrowers for the harm caused by these unfair denials. This case is ongoing, but it highlights that legal action is underway and could pressure Navient to improve its practices or grant more discharges.

Tip: Even if you don’t currently have a lawyer, keep notes of every interaction with Navient (phone calls, etc.). If Navient representatives ever told you that you cannot discharge a private loan due to school fraud, or discouraged you from pursuing it, note that down – that could be evidence of misleading communication. (The CFPB has noted that servicers often “misled borrowers about their right to challenge their loans” in such cases.)

Another avenue is to raise your voice with the regulators and watchdogs:

When filing complaints, be concise and factual. State what the school did (e.g. false claims, high-pressure sales tactics), that you have a private loan from Navient as a result, and that Navient is refusing to honor your right to discharge despite evidence. Emphasize if you have supporting documentation or if the school’s misconduct has been publicly documented (for example, “my school was later investigated by the state for fraud” or “ED approved borrower defense discharges for students of my school, but I’m stuck with a private loan”).

Important: This is not a recommendation, but rather a discussion of a difficult option. Stopping payment on a private loan (i.e. going into default) is risky: it will harm your credit, the lender may send the loan to collections or sue you, and if you have a cosigner, they’ll pursue them too. However, some borrowers in extreme circumstances do choose to strategically default as a last resort, especially if they are judgment-proof (no income or assets to garnish) or the debt is truly unpayable. The sad reality is that the 2022 Navient settlement only helped those who were severely delinquent/defaulted – effectively rewarding non-payment. Borrowers who made good-faith payments got left with the bill. This creates a moral hazard where defaulting can seem like the only way to eventually get relief.

If you do find yourself unable to continue payments, know your rights in default. You will have the opportunity to raise defenses if the lender or a collector sues you. This is where the Holder Rule defense comes in most directly: in court, you can assert that the debt is not collectible because of the school’s fraud. You might need a lawyer’s help to do this effectively. Courts have in some instances sided with borrowers who proved school fraud, canceling the debt. The downside is you’d have to endure collections and legal proceedings to get there.

A potential middle ground is attempting to negotiate with Navient (or whatever entity holds the loan) for a settlement. If you have evidence of wrongdoing, you might say, “I intend to contest this debt due to the school’s fraud and have alerted regulators – would you agree to discharge or settle for a lesser amount to avoid further action?” This approach can be hit-or-miss; some borrowers have had loans quietly forgiven after raising hell, while others get nowhere. Navient did reserve $35 million in late 2023 for potential discharges due to “borrower claims”, indicating they expect to forgive at least some loans. It’s not a lot of money relative to all loans, but it’s something.

Caution: If your loan is still within the statute of limitations for collection and you have means they can go after, default is generally a last resort. Always consider consulting an attorney before deliberately withholding payment.

Many people believe student loans cannot be discharged in bankruptcy, but that’s an oversimplification. Federal student loans and most private student loans are indeed hard to discharge because of a law that requires proving “undue hardship” (a tough standard) in court. However, some private loans are not covered by that strict standard. For a private loan to be protected from discharge, it generally must be a “qualified education loan” – which means it was used at an eligible institution and for qualified expenses (tuition, etc.). If your school was unaccredited or your loan exceeded the cost of attendance or was for something like bar exam prep, that loan might not meet the definition of an education loan in bankruptcy law. In those cases, the loan could be treated like regular unsecured debt and discharged through bankruptcy without the undue hardship test.

Even if your loan is a typical private student loan from an eligible school, bankruptcy is still an avenue if you can meet the hardship test (the Brunner test in most jurisdictions, which requires showing persistent financial difficulty, good-faith effort, and a hopeless outlook for repayment). There have been instances of courts discharging private student loans for borrowers from predatory schools, especially when the education provided no value and the debt is crippling. Some judges are becoming more sympathetic in egregious cases of for-profit fraud.

Recent developments: There is growing bipartisan support to make student loan discharge in bankruptcy easier. Legislation has been proposed (e.g. the Fresh Start Through Bankruptcy Act) that would explicitly restore the ability to discharge student loans (including private loans) after a certain number of years or without the harsh tests. As of 2025, no such bill is law yet, but keep an eye on Congress. If the law changes, bankruptcy could become a more viable tool for relief.

Note: Bankruptcy is a serious step with broad implications on your finances, so consult a bankruptcy attorney to evaluate your specific situation. But if you’re truly unable to pay and other relief hasn’t materialized, it’s worth exploring – especially if you suspect your loan might not be the kind Congress intended to shield (given it was part of a fraudulent scheme).

Beyond your individual case, it can be empowering and useful to connect with the larger movement of borrowers and advocates dealing with these issues. Organizations like the Project on Predatory Student Lending, the Student Borrower Protection Center, and various borrower advocacy groups regularly publish updates, host webinars, or provide resources. For example, PPSL has a resource hub for Private Student Loans and has been pushing for systematic solutions. They even helped prompt the awareness campaign about Navient’s secret discharge program by publicizing the application form and alerting media.

Why engage? Sometimes, collective pressure leads to change. The more stories and complaints that come out, the more likely regulators or legislators will step in. Media coverage (such as the New York Times piece that broke the news on Navient’s program in May 2024) can spur action. Consider sharing your story (carefully, without exposing personal data) with reporters or through platforms like the CFPB’s “Tell Your Story”. Lawmakers (like Sen. Warren or your own representatives) often invite constituents to share if they’ve been harmed by student loan practices – adding your voice can prompt letters, hearings, or inquiries that benefit everyone in your situation.

The landscape for borrower protections is evolving. Here are some key things to watch in the near future, which could affect your options:

To distill all of this into actionable steps, here’s what you (as a borrower dealing with this) can do right now and in the near term:

In closing, know that you do have rights and potential avenues for relief – even if Navient’s current stance is hostile. The legal system and regulators are slowly catching up to this problem. As frustrating as it is, persistence can pay off. We’ve seen waves of relief for federal loan borrowers from predatory schools; now the focus is turning to private loan borrowers like you who were unfairly burdened. By staying informed and assertive, you increase your chances of being in the next wave of relief – whether through a successful application, a court judgment, or a policy change.

The highest level of education and consulting in Borrower Defense for Student Loans.

Legal Touch Borrower Defense - Copyright . All rights reserved. Designed by Explore Logics